The Truth About Angel Investing (Part III)

Best Practices

Angel Thoughts

What follows is a members-only post for Vertical members where we discuss trends, thoughts, lessons, best-practices, and other entertaining nonsense about angel investing. Since our members sit at the intersection of technology and real estate, we are always trying to learn about what is happening at the earliest-stage of startup investing.

If you were forwarded this and would like to become a member and have access to other posts and discussions like this, join the conversation here.

Otherwise, read on, leave a comment, and tell me what I missed.

We’ve talked about misconceptions and we’ve discussed how to get started with angel investing. Before we get into a few predictions, let’s talk about some best practices.

So now you’re an angel investor. Congrats!

Angel investing is the most educational use of your time besides starting your own company.

But, your time and capital are finite and valuable.

How much time should you spend on this? How deep should you go into due diligence? How much diversification should you aim for?

These are the questions that generally pop up once you officially get “into the game” and start angel investing with regularity.

So, let’s dig into to these and work out some best practices I have learned.

First, frame how you can help a startup.

One truth of startup investing is - the best ones are the hardest to get into.

This should intuitively make sense. Founders who have personal capital and track record don’t need your capital. They already have both and angels will line up to invest with them.

If you, presumably not a close friend of this buzz-worthy founder, want to get on her cap table, what are you going to help her with?

You should have already been thinking about this in Getting Started, but now I want you to formalize and codify (in writing) this concept. You should be able to tell founders why you would make a great addition to their cap table. The founders who know they should care about that are the people you actually want to invest in.

Having it in writing will help you make it punchy and compelling. Edit and update this over time as your network and skill set grow.

Best Practice 1 - Codify how you help founders and their companies.

Second, ask yourself what your main goal is with your angel investing.

If you goal is to maximize your return, then I would recommend making as many investments as possible. Some people say 10 minimum and some have said 30 minimum to ensure you pick a few “winners” and learn the best practices. That’s a good range.

That should give you the diversification you need and give you access to plenty of impressive founders.

If your main goal is to learn, I would only try to invest in the handful of companies with the most remarkable founders that are aligned with your thesis and niche. Go “deep” with those companies and get as involved as possible. You’ll learn just by proximity to these impressive founders.

Most investors would like a mix of both: Education + ROI.

If that’s the case, think about having a hybrid model of investing directly (via AngelList or through a group) and investing in rolling or traditional funds in your niche, if your net worth will allow.

Direct investing will give you direct access to the founder. Rolling Funds will give you some diversification which should boost your returns (if you pick the fund manager correctly). **Note - I will assume you know what rolling funds are and how they work, but feel free to shoot me a note if not.**

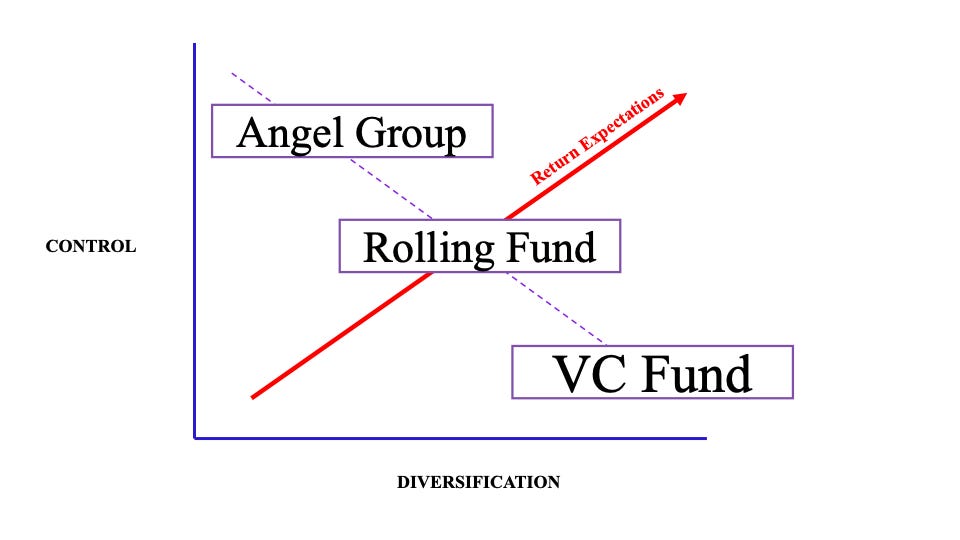

Also, I put together this illustration to show you how you should think about the trade-off between diversification and control in the startup investing arena.

The idea is - the further you move to the right, the less control you have but the more diversification you have. In a VC fund, you have no control but high diversification. In an angel group, you have complete control but little to no diversification. Rolling Funds are somewhere between the two.

So, know what you are aiming for and align your strategy around the amount of control and diversification you want.

Best Practice 2 - Set up an investment strategy aligned around your main goal(s).

Third, find a diligence sweet spot.

I was trained in private equity and diligence was/is my craft. I can go down rabbit holes and spend weeks analyzing weaknesses and mitigants. My last memo on an angel deal was more than 20 pages.

That’s probably overkill. But I can’t always help it.

So what you need to figure out is where your diligence sweet spot is for an angel deal. Because I can promise you that you will never have perfect or complete information. You’ll ALWAYS have to make an investment decision based on partial information.

Get comfortable with that and decide what your definition of “sufficient” information is with your capital.

Some angels prefer face time with the founder(s) on multiple calls/Zooms/coffees. Some are fine with co-investing with other angels whose diligence they trust. It’s your call, but it has to dovetail with your schedule.

If you’re only comfortable with long, 20-page diligence analysis of startups and are investing part-time, don’t expect to do many deals or do them quickly. That’s going to take a ton of your nights and weekends.

So be sure to incorporate your schedule and analysis sweet spot into your plan for angel investing.

Best Practice 3 - Find your diligence (and therefore time commitment) sweet spot.

Fourth, learn how to identify and work with co-investors.

You will not always be the first one to find interesting deals. Others will surface cool deals on AngelList and ask you to join their syndicate.

You need to cultivate the ability to identify gifted or thoughtful co-investors.

Whether they lead a deal or you want to bring them into a deal that you lead, you’ll need to eventually grow a rolodex of co-investors. That will feed back into BP1 above and how you add value to startups.

There are several ways to do this but I hesitate to make any strong recommendations here because it is highly personal. Some people really like to invest with other angels who focus on ESG and sustainable investments. Some just want to coalesce with angels that support woman and minority founders.

Whatever you prefer, solve for that, work AngelList and LinkedIn, and form your tribe. I can’t make your criteria for you, but I can recommend that you develop a keen eye for finding others who value what you value.

Best Practice 4 - Learn how to identify and work with high-quality co-investors.

Fifth, commit to learning.

Too many people underestimate investing.

I see it all the time. Founders conflate starting companies with investing in companies. Investors conflate investing in public or private equities with investing in startups.

Startup investing is its own craft and skill.

Name a skill you are great at that you didn’t have to learn about and practice extensively.

I’ll wait . . .

If you want to be great, you need to take time to learn about it.

To start, I would recommend reading Jason Calacanis’ Angel. For all his grandstanding and bragging, Jason does do a great job of explaining the essentials of angel investing and why it’s interesting/important/educational. You’ll learn from his book. So look past the ego and take the ideas.

I’d also recommend the encyclopedic Venture Deals. It’s terrific, if a little dense. Maybe I should say that twice as a fair warning - it can be a grinding, detailed read. But if you want to understand venture deals at a deeper, longer-term-consequence level, you need to read it. You’ll come to appreciate all the terms and clauses that your portfolio companies will be subject to and how they can come in to play in the future.

From there, just keep your eyes and ears open for books, online courses, mentors, and co-investors you think you can learn from. The quality will obviously vary and beware of anyone looking for large sums of money trying to teach you to angel invest. (It’s probably not worth it.) There are digital reams of writing on angel investing and you can synthesize it if you simply commit the time to learning it.

If this is a life-long commitment, you must have a plan for your education.

Best Practice 5 - Commit to learning.

Bonus: Get involved in the VC community.

If you picked your niche and thesis well in Part II, you will probably find that a few VCs consistently pop up investing “down stream” from you.

Take note of who they are and find a way to meet them.

This will serve two purposes. First, you’ll know what professional investors are looking for in startups a little later than you invest. That will help you identify the types of startups with staying power in your niche.

Second, it’s a good defense strategy.

If you read Jason’s book, you’ll hear a story about him being an early advisor/angel to a buzzy startup and eventually getting booted off the cap table by a VC. This happens more than you think and having a relationship with the VCs in your niche will help prevent it (as much as possible). Simply put, if VCs see you as a consistent source of deal flow and info, they will not be incentivized to screw you and dilute your shares to $0.

Know the players down stream and you are less likely to get in trouble when they start flirting with your portfolio companies.

Bonus - Know the VCs in your niche.

To summarize, once you know what angel investing is and what it is for, you need to:

Codify how you help founders and their companies.

Set up an investment strategy aligned around your main goal(s).

Find your diligence (and therefore time commitment) sweet spot.

Learn how to identify and work with high-quality co-investors.

Commit to learning.

If you can create a system that incorporates those 5 best practices, you will be in the top 1% of angels on the planet regardless of your new worth and check size. And if you can form meaningful relationships with VCs, you’ll be positioned to keep your place on the cap table of your break-out winners.

Next time, we’ll explore some predictions about the future of angel investing, its platforms, and consequences. Don’t miss it.

And, if you want exclusive content, happy hours, and our private community, consider becoming a member of our Vertical Community.