The Tip of the PropTech Spear

Aggregating the best tech adopters in the Goldilocks Zone

When you spend enough time in the world of real estate innovation, you learn that not all customers are created equal.

That may seem obvious on the surface but I see this mistake being made over and over and over again by young startups chasing huge customers.

I’m going to explain why it’s a mistake and I’m actually building something to fix it.

The nuances of Ideal Customer Profile (“ICP”) are vast and a topic for another post. For this discussion, let’s agree that each startup selling tech into the real estate ecosystem MUST identify who her ideal paying customer would be if she has any hope of creating a sales pipeline to convince a buyer to, well, buy.

If you aim at nothing, you’ll hit it (as they say).

So, it’s pretty basic business logic that anyone selling anything needs to give nuanced thought and wisdom into whom they target.

In the chase for $100M or $200M in sales, startup founders often assume that “bigger is better.”

The logic goes - Why go after mid-market homebuilders when I go just as easily go after a top-10 homebuilder for my pilots?

Why go after a top 500 property manager when I could work with a top 5 manager?

The big guys have bigger balance sheets, more projects/properties, and therefore represent more potential revenue for the fledgling startup.

In theory, that is true. In practice, it almost never works out that way and I would argue that it is precisely the wrong approach for a young startup.

Many startups boast of a huge partnership with (insert large/famous company here). They show off the logo on their website as “Current Partner”, post an announcement on LinkedIn, and think it will lead to TONS of other sales from the companies that want to be just like large/famous company.

It almost never does.

In reality, this approach can be financially catastrophic for a young startup.

I can’t tell you how many startups I’ve seen that ran out of cash waiting for a large company to approve or pay for a pilot.

It’s like fisherman starving to death because they spent all their time whale-hunting.

There are plenty of other fish to eat and companies to work with.

My argument is that there is a sub-sector of the real estate world I call “The Goldilocks Zone” that is ideal for revenue-starved startups to target as sales prospects and it is certainly NOT the largest, sexiest companies in our space.

It’s the Emerging Manager.

In this context, an Emerging Manager is just an up-and-coming real estate owner, operator, builder, or developer.

Everyone defines the term a little differently and I will give mine below but the basic sweet spot is this:

Big enough to have a tech budget and small enough to say yes (or no) in a week.

That’s our sweet spot. That’s Goldilocks’ just right choice. That’s who should make up the bulk of your sales pipeline when you are starving for revenue.

In the fishing analogy, it’s like reeling in some cod, sea bass, and maybe a tuna or two before you go after the whale.

Here is how I define them by asset class -

Multifamily: 2,000 to 8,000 units, give or take

Office: 1M > 4M SF under management, probably $20M in NOI

Industrial: >1M SF, probably $10M in NOI

Retail: >1M SF

Hotel: To Be Defined

Homebuilder: To Be Defined

I kept these definitions to owners and builders but the same logic could apply to general contractors, brokerages, appraisers, lenders, etc. In every corner of real estate, you have this sweet spot goldilocks zone where the company is big enough to have a tech budget and innovation person while still being small enough to be quick and decisive.

These firms are hungry for growth and will pursue any (ethical) strategy to obtain it - including tech leadership.

Can you imagine a better customer than one who is both hungry for tech and decisive when approached by tech companies?

I can’t.

So, if they are the “tip of the spear” when it comes to PropTech adoption, why aren’t they all the rage at trade shows, LinkedIn posts, investors updates, etc.

Simple - they are hard to find.

Google - “Emerging Managers in Real Estate”

What did you find?

See how it’s a bunch of definitions, conferences, paywalled databases, etc. You can see several large LPs like CalPERS that have programs to invest in these up-and-comers but you rarely get a list of the actual firms and their portfolios.

So we created one.

More precisely, we are in the process of creating one.

Coming from CRE myself, many of my friends and former colleagues fit this definition. So I started putting together a crew.

Then I realized that Brad at Thesis Driven had a huge developer database and lots of these connections himself.

So, we partnered with Brad and his team.

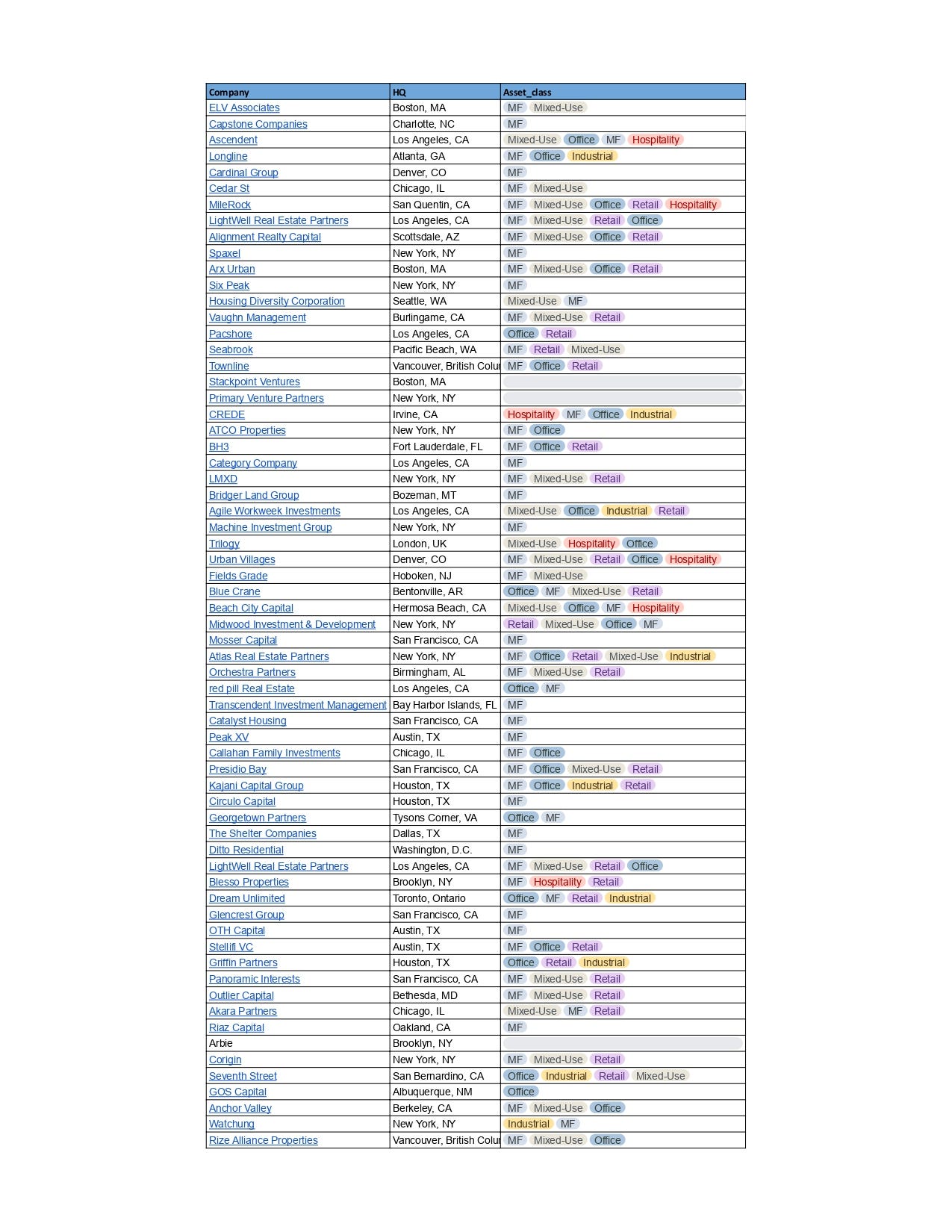

As of now we have put together about 75 emerging managers that we are coalescing to discuss technology, best practices, pilots, costs savings, and whatever else keeps them up at night.

The first group looks like this:

We have a slack channel, regular calls, free legal documents, tickets to events, and more.

The idea is that we can get this group together to be proactive and decisive on their tech strategies and that will equate to more pilots for them, more revenue for startups, better pricing for their tech stack, better collaboration between firms, and more.

Should be fun.

So I have two asks of you -

More emerging managers

We always need more high-quality members. As of right now, this is a completely free resource for firms/people who qualify. Eventually, it will be for FIRE donors only but it’s free as of now. Please send me your favorite up-and-comers and I’ll get them plugged in.

Ideas

What would make this group most useful and effective? Any ideas on partnerships or ways to expand?

If we do this right, it has the opportunity to be the go-to group of early adopters in PropTech. That’s an extremely powerful concept.

We have a long way to go to get there but this is the right group of people to do it with.

Anything I missed?

To learn more about FIRE and all of its programs, visit here.

And please consider donating to us so that we can continue building impactful programs like this one.